Mobile wallets are making headlines these days. Domestic e-commerce companies, such as Flipkart, plan to launch a wallet soon, while a few payment gateways, such as Paytm and Mobikwik, offer semi-closed wallets already. Telecom operators also offer this facility. Internationally, too, Apple Inc. is said to be introducing an iPhone wallet on 9 September, which will have tie-ups with Visa Inc., MasterCard Inc. and American Express Co.

According to many experts, mobile wallets are going to be the next wave of change in the way people make payments.

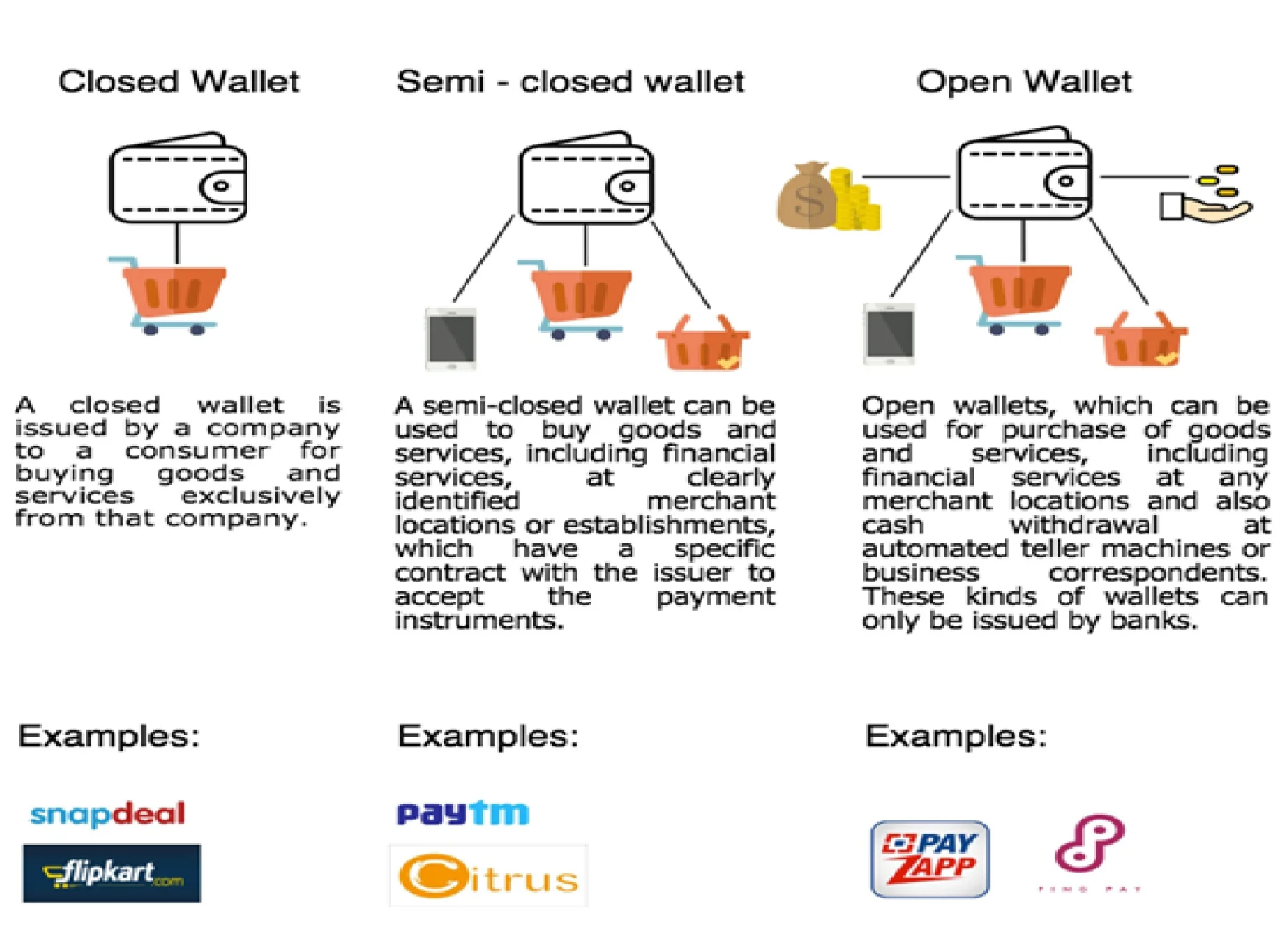

Simply put, it is a virtual money wallet that can be used to make instant payments, same as with a physical wallet. It is an application stored in cellphones, which enables users to make payments for utility bills, book tickets, transfer money and other such transactions. It can also be used to make instant e-payments while shopping, in physical stores or at e-stores.

Three types of mobile wallets:

Eligibility

Only bank are allowed to issue all kinds of wallets including open wallet. NBFC’s and other persons can issue only closed and semi closed wallets.

Permission from RBI

Entities issuing closed prepaid payment systems are not required to take the authorization from RBI, they just need to inform the RBI. Entities issuing semi closed and open prepaid payment systems are required to take the authorization from RBI.

Law governing mobile wallets

The Payments and Settlement Systems Act, 2007 is the primary law governing payments systems in India, with the RBI as the body to supervise related matters. Section 18 of the Act empowers the RBI to make such regulations as may be required, from time to time, to regulate payments systems in India. In exercise of the same, the RBI has laid down guidelines for the issuance and operation of Pre-paid Payment Instruments. A Master Circular consolidating all regulations on the same was notified on July1, 2014.

Other Requirements

A company (that which is not a bank or a NBFC) seeking RBI’s authorization should have a minimum paid-up capital of INR 5 crores and a minimum positive networth of INR 1 crore at all times.

The Circular specifies anti-fraud mechanisms/standards and the level of Customer Due Diligence required based on the quantum of transactions involved. KYC norms and Anti Money Laundering norms, as relevant would continue to apply to pre-paid instruments. Importantly, these regulations do not cover any cross border transaction and do not extend to any foreign exchange pre-paid instruments allowed by RBI under FEMA.